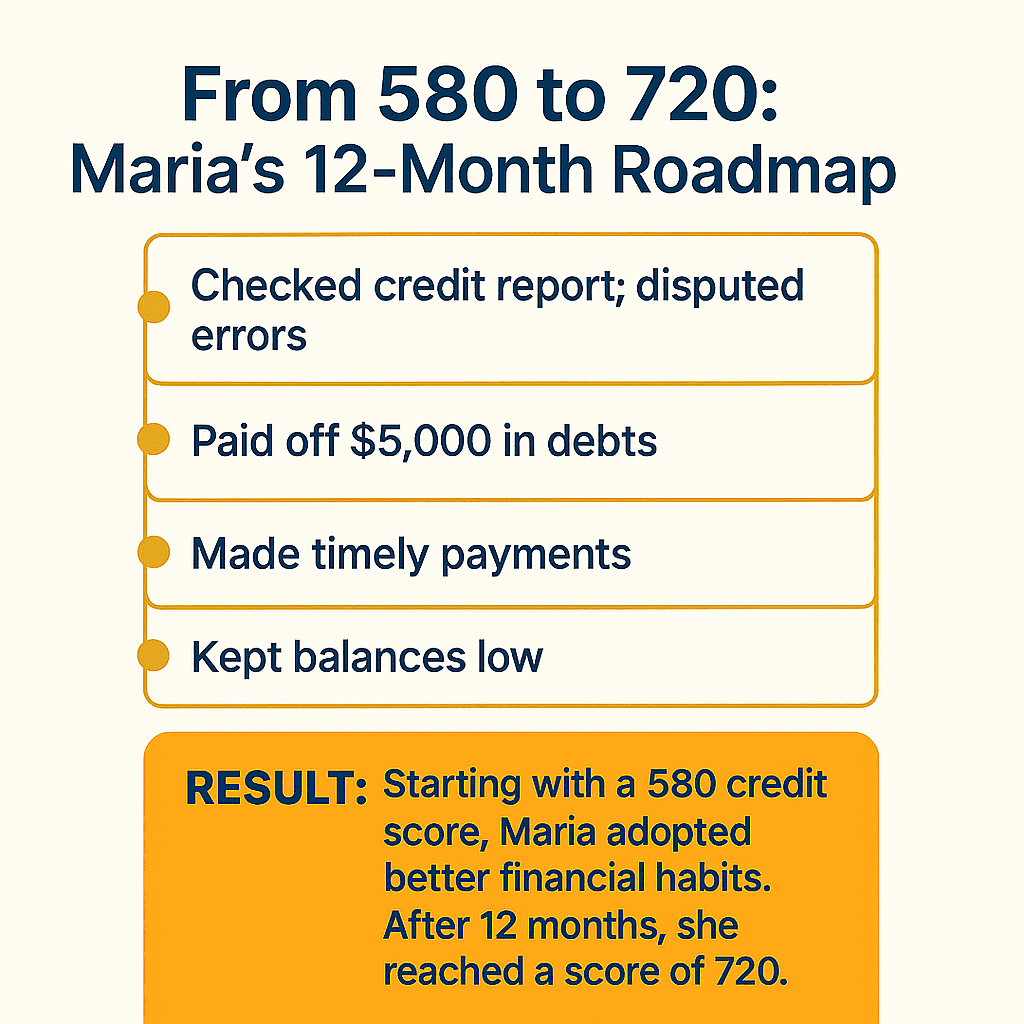

From 580 to 720: Maria’s 12-Month Roadmap

Maria is a single mom and a nurse in San Antonio, Texas. When she called me in early 2023, her voice was shaking.

“I’m stuck at 580. I’ve paid off some things, but nothing seems to help. My landlord’s raising the rent. I need to buy a home.”

That conversation turned into a yearlong plan. And by March 2024, Maria had a 720 credit score — no expensive “credit repair” company, no lawyer, no gimmicks.

Here’s exactly how we did it, month by month.

Month 1–2: Clean the Slate

- We pulled all three credit reports using AnnualCreditReport.com — for free.

- Found one collection ($122 from an old phone bill). She called the agency and negotiated a pay-for-delete.

- Sent certified letters disputing two inaccurate late payments from 2020. One was removed.

“I didn’t even know those were still showing,” she told me.

Most people don’t.

Month 3–4: Build the Right Habits

Maria had 2 credit cards — both nearly maxed out.

- She picked up a weekend shift to put an extra $150/month toward paying down balances.

- We focused on bringing each card under 30% utilization.

- I coached her to pay before the statement date, not just the due date. That trick alone gave her a 20-point boost.

Month 5–7: Add Positive Credit History

Maria was “thin file” — not much recent credit activity.

- We opened a secured credit card with a $300 deposit.

- She charged $30–$40 each month and paid in full.

- I also helped her apply for a credit builder loan through her local credit union.

At Month 6, her score hit 640. She cried. “I’ve never been over 600 before,” she said.

Month 8–10: Let Time Work

Now that her profile was stabilizing, we did… nothing flashy.

- Kept all cards under 10% utilization.

- No new accounts.

- Auto-paid every bill.

FICO likes boring. Credit growth rewards consistency, not drama.

Month 11–12: Final Boost

With on-time payments and low balances, her score kept rising. At Month 12:

- All 3 reports clean

- Utilization at 7%

- Credit mix improved

Her FICO score was 720.

She was approved for a first-time buyer mortgage — 3.5% down, no co-signer.

What Maria Taught Me (Again)

Credit repair isn’t about tricks — it’s about discipline. She didn’t make more money. She made better moves.

“I used to think people like me just couldn’t have good credit,” she told me.

“Now I feel like I have options.”

That’s the goal. That’s the roadmap.