Credit Freeze vs Credit Lock: Which One Should You Use and When?

When Cheryl got a notice about a new loan application in her name, she panicked. She hadn’t applied for anything.

“Should I freeze my credit or just lock it?” she asked.

That question is more common than you’d think — and the answer depends on how much protection and control you really want.

Let’s break it down.

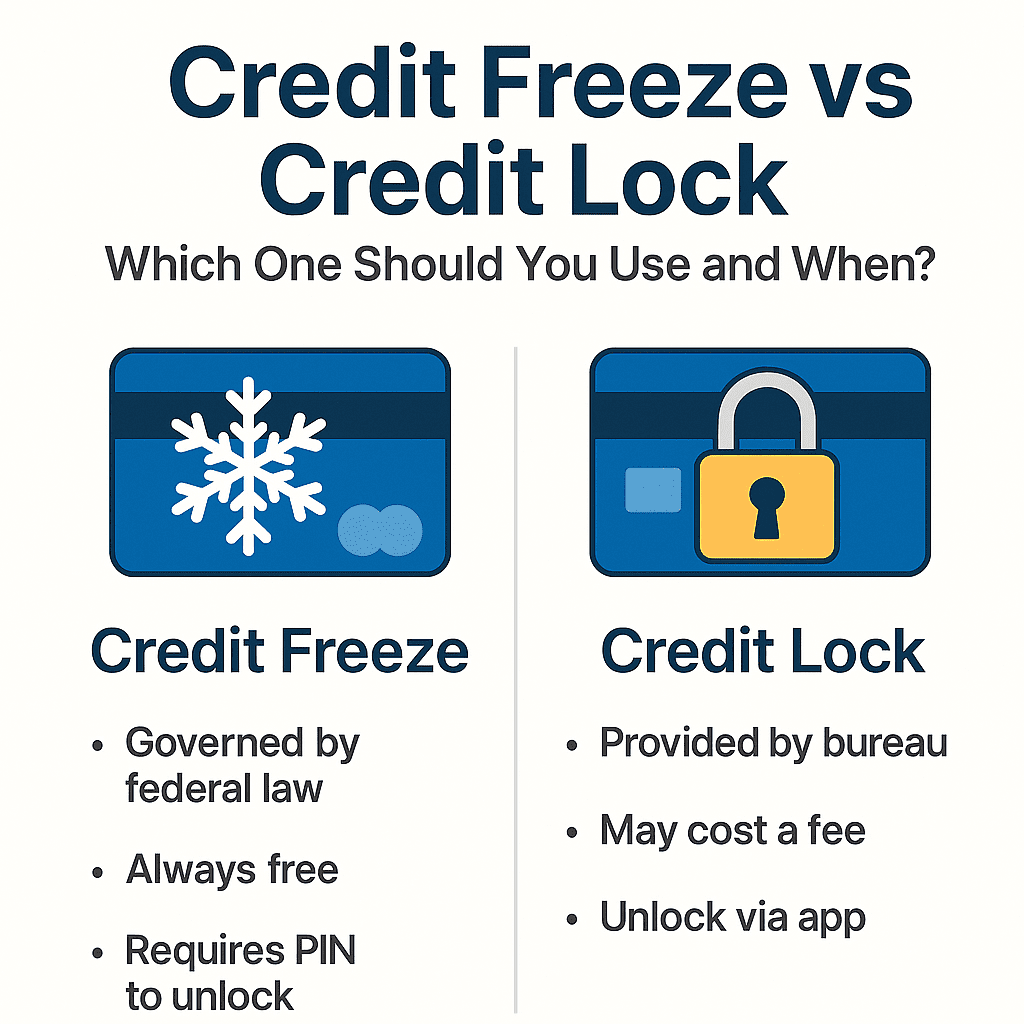

🔐 What Is a Credit Freeze?

A credit freeze is a federally mandated tool that stops lenders from accessing your credit report entirely. It’s powerful, simple, and free.

- Governed by federal law

- Always free from all three bureaus

- Requires PIN or login to lift the freeze

- Does not affect your current credit lines or score

Best for:

- Victims of identity theft

- People not planning to apply for credit soon

- Long-term security

🔒 What Is a Credit Lock?

A credit lock is a similar concept — it blocks access to your credit file — but it’s managed by the credit bureaus themselves.

- Offered through mobile apps or online portals

- Sometimes part of paid identity protection services

- Easier to toggle on/off

- Not legally protected like a freeze

Best for:

- People who apply for credit often

- Those who want convenience over legal guarantees

📊 Quick Comparison

| Feature | Credit Freeze | Credit Lock |

|---|---|---|

| Legal Protection | ✅ Yes | ❌ No |

| Free to Use | ✅ Always | ⚠️ Sometimes |

| Easy to Toggle | ❌ Not Instantly | ✅ Via App |

| Best For | Strong security users | Frequent applicants |

🧠 So, Which One Should You Choose?

If you’re dealing with fraud or just want to lock things down — go with a freeze.

If you want flexibility and instant access — a lock might be your style.

“I went with the freeze,” Cheryl told me later.

“And the peace of mind was worth it.”